The Coronavirus Aid, Relief, and Economic Security (“CARES Act”) is a $2 trillion emergency bill that Congress prepared in response to the Coronavirus (COVID-19) pandemic. The Senate passed the bill on March 25, 2020, followed by passage in the House on March 27, 2020. President Trump is expected to sign with little delay.

Many provisions in the bill are designed to provide financial relief to individuals and small businesses. Below is a summary of the most impactful areas and how they may affect you as a small business owner or individual taxpayer.

This article outlines four major components:

- The Paycheck Protection Loan Program

- SBA Loan Relief

- Tax Incentives

- Unemployment Insurance

Paycheck Protection Loan Program

The CARES Act creates a Paycheck Protection Program for small employers with 500 employees or fewer, participants who meet existing Small Business Administration (“SBA”) size guidelines, self-employed individuals, gig economy workers, and certain nonprofits.

The goal is to prevent layoffs and business losses caused by the COVID-19 crisis. The program offers eight weeks of cash-flow assistance through federally guaranteed loans for employers that maintain payroll. If payroll is kept intact, the portion of the loan used for eligible expenses — payroll, mortgage interest, rent, and utilities — will be forgiven.

This provision is retroactive to February 15, 2020 to encourage rehiring workers who may have already been laid off.

Special Loan Terms

The Paycheck Protection Program significantly expands access to SBA loans for necessary operating expenses, including payroll, paid leave, insurance premiums, and rent or mortgage payments. Key features include:

- The loan size equals 250% of average monthly payroll

- Covered payroll costs include salary, tips, health care benefits, insurance premiums, retirement contributions, and leave

- Loan maximum of $10 million

- No fees, prepayment penalties, or loan origination costs

- Automatic payment deferment for six to twelve months

- Loans available through 800+ existing SBA-approved lenders

- Fast expansion to additional lenders to expedite financing

Loan Forgiveness

Borrowers are eligible for loan forgiveness equal to the amount spent during the first eight weeks on payroll, mortgage interest (incurred before February 15, 2020), rent (active prior to February 15, 2020), and utilities (service started before that date).

Forgiveness cannot exceed the principal amount and excludes payroll compensation over $100,000. Forgiveness will be reduced if a business reduces staff or cuts wages more than 25 percent compared to the prior year.

Employers rehiring previously laid-off employees will not be penalized for early reductions.

Forgiven debt is not counted as taxable income.

SBA Loan Relief

The CARES Act provides $17 billion for small business loan debt relief. For six months, the SBA must pay principal, interest, and fees on all existing SBA “covered loans,” including 7(a), 504, and microloans.

Loans already in deferment will receive six months of SBA payments following the existing deferral period. Loans issued within six months of enactment will also qualify.

The SBA is required to implement these provisions within 15 days of the bill being enacted.

Tax Incentives

One-Time Financial Assistance

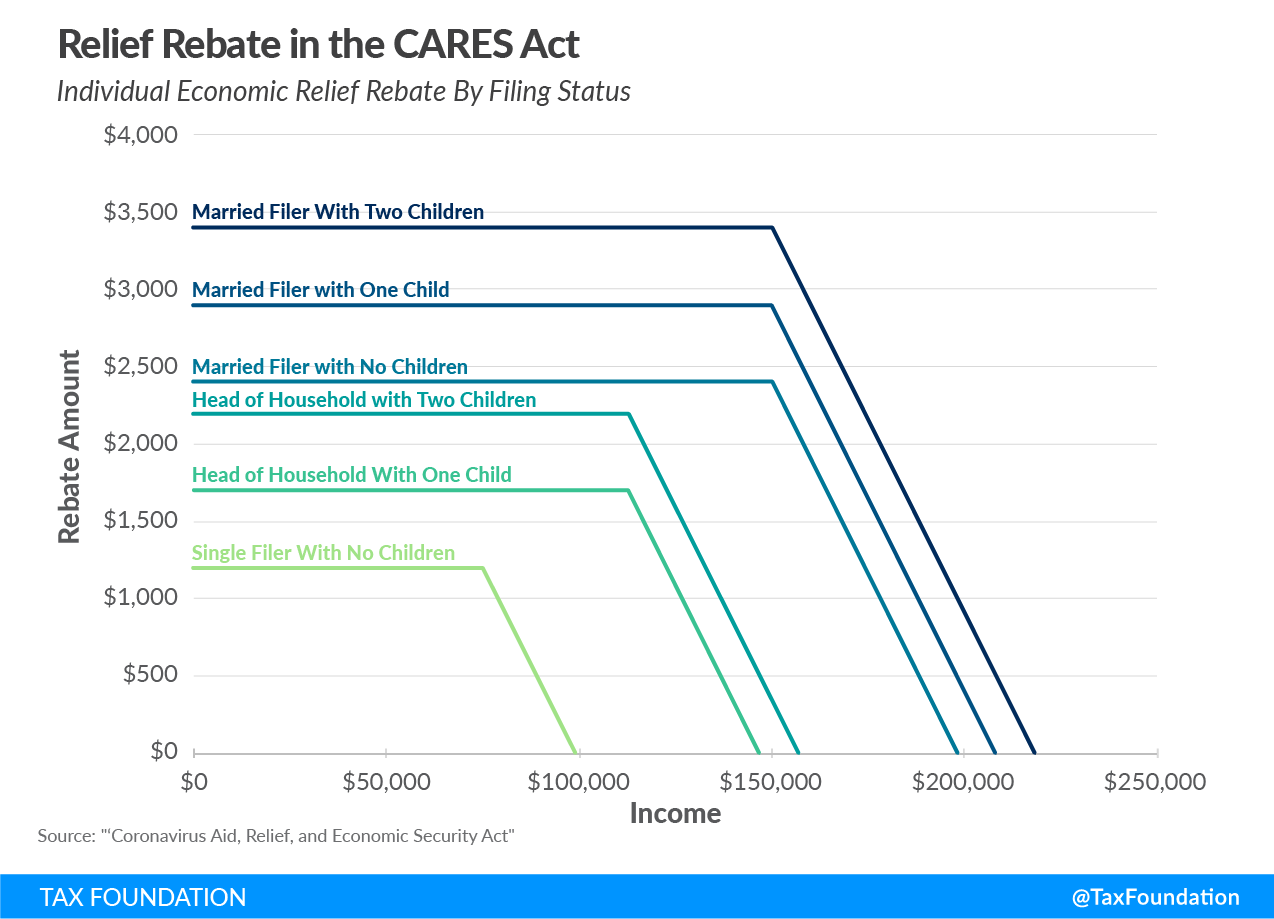

Individuals will receive a one-time rebate of $1,200 plus $500 per qualifying child. There is no income or tax liability minimum.

Full payments go to individuals earning up to $75,000 ($112,500 for heads of household and $150,000 for married couples). Benefits phase out fully at $99,000 for single filers and $198,000 for joint filers with no children.

The IRS will use 2019 tax returns (or 2018 if not filed) to calculate payments. Any underpayment will be corrected when filing 2020 taxes; overpayments will not be clawed back.

Relaxed Rules on Retirement Distributions

Required minimum distributions (RMDs) for 2020 are suspended, allowing retirement accounts to remain invested.

The 10% penalty on COVID-related early withdrawals from IRAs and 401(k)s is waived for 2020. Tax owed may be spread over three years, and withdrawals may be recontributed within three years without impacting contribution limits.

Payroll Credit for Furloughed Workers

Employers may claim a refundable payroll tax credit of 50 percent of wages paid (up to $10,000 per employee). Eligible businesses include those shut down due to government orders or those experiencing a 50 percent revenue drop compared to the same quarter last year.

Large employers (100+ employees) may claim the credit only for wages paid to workers not providing services. Smaller employers may claim all wages paid.

Payroll Tax Payment Deferral

Businesses may delay payment of employer payroll taxes until 2021 and 2022. Half of the deferred amount is due December 31, 2021, and the remainder on December 31, 2022.

Student Loan Assistance

Employer-paid student loan contributions of up to $5,250 annually are excluded from employee income in 2020.

Net Operating Loss (NOL) Flexibility

Businesses may carry back NOLs from 2018, 2019, and 2020 to the prior five years and fully offset taxable income, temporarily removing the 80 percent limitation.

Encouraging Capital Investment

The Act corrects depreciation rules for Qualified Improvement Property (QIP), enabling businesses with QIP expenses in 2018 and 2019 to claim refunds now.

Expanded Net Interest Deduction

The business interest deduction limit temporarily increases from 30 percent to 50 percent of EBITDA for 2019 and 2020, improving liquidity for debt-burdened businesses.

Unemployment Insurance

The CARES Act allocates $250 billion to expand unemployment benefits. Recipients receive an extra $600 per week for up to four months.

Benefits now extend to independent contractors, self-employed workers, gig workers, and those with limited employment history.

States will receive full federal funding to cover the first week of benefits and may offer an additional 13 weeks beyond standard state benefits.

State and local governments and nonprofits may pay unemployment for their employees under these provisions.

How We Can Help

As provisions roll out, our team is here to assist you with understanding and applying the programs and credits available to you. Contact one of our advisors to discuss how the CARES Act impacts your situation.

Sources

Garret, W., LaJoie, T., Li, H., Bunn, B., Tax Foundation 2020.

https://taxfoundation.org/cares-act-senate-coronavirus-bill-economic-relief-plan/

U.S. House of Representatives: Ways and Means, 2020.

https://gop-waysandmeans.house.gov/the-senate-cares-bill-helping-small-business/

National Small Business Association.